.png)

Source: Bloomberg, MSCI, Standard & Poor’s, J.P. Morgan Asset Management. Shows initial drawdown to the trough and recovery since. U.S. Equity: S&P 500, EM Equity: MSCI EM, DM Equity: MSCI EAFE, High Yield: Bloomberg U.S. Corp. HY, IG Corp.: Bloomberg U.S. Corp., 2Y Treasury: Bloomberg U.S. Treasury 2Y TR, 10Y Treasury: Bloomberg U.S. Treasury 10Y TR, Gold: XAU.

Geopolitical tensions, inflation concerns, and tariff uncertainty dominated financial headlines throughout the second quarter of 2026. As conflict escalated between Israel and Iran, many analysts warned of a potential global recession, surging oil prices, and renewed inflationary pressure. Yet despite these fears, markets once again demonstrated resilience.

The S&P 500 experienced volatility during the height of the conflict but avoided entering official correction territory, ultimately rebounding to new all-time highs by late April. Strong corporate earnings, continued consumer spending, and ongoing artificial intelligence investment helped support equity markets even as headlines remained overwhelmingly negative.

As the quarter progressed, investors were once again reminded that headlines and long-term market outcomes are often very different. Understanding the underlying fundamentals driving markets remains critical in navigating periods of uncertainty.

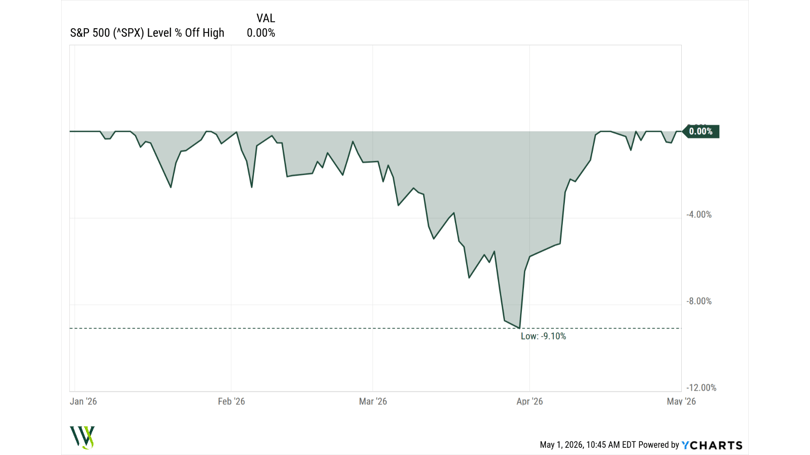

Volatility Returned, but Markets Stayed Resilient

Market volatility increased sharply during the early stages of the Iran conflict, with the S&P 500 falling roughly 9% from its highs as recession fears intensified (as of May 1st, 2026). Many forecasts projected prolonged economic weakness tied to rising oil prices and geopolitical instability.

Despite those concerns, markets recovered quickly. April became the strongest month for the S&P 500 since 2020, and by late spring the index had resumed setting new all-time highs. Historically, periods of sharp short-term recoveries have often been followed by positive long-term returns, reinforcing the importance of maintaining discipline during volatile periods.

Importantly, the pullback experienced this quarter remained well within normal historical ranges. Market corrections and temporary declines occur regularly, even during strong long-term bull markets, and are not unusual on their own.

Past performance is not indicative of future results. This report has been generated through application of the analytical tools and data provided through ycharts.com and is intended solely for conducting investment research. The investment examples set forth in this presentation should not be considered a recommendation to buy or sell any specific securities. There can be no assurance that such investments will remain in the strategy or have ever been held in a WJW strategy. For discussion purposes only, not for external distribution.

Energy Markets and Inflation Pressures

One reason the economy absorbed the Iran conflict more effectively than many expected is that the U.S. economy is structurally different than it was during prior oil crises. The United States is now a net exporter of petroleum products, reducing overall vulnerability to energy shocks compared to previous decades.

In addition, household energy costs consume a smaller share of consumer spending today than during the inflationary periods of the 1970s, 1980s, or even the 2008 commodity spike. Although oil prices moved higher during the conflict, the broader economic impact remained more manageable than many feared.

Inflation has nevertheless ticked higher in recent months, with headline CPI rising to approximately 3.8% in April. While inflation remains well below the 2022 peak of 9.1%, higher energy prices remain an important variable to monitor moving forward.

Inflation Has Cooled, Even If It Doesn't Feel Like It

Inflation peaked at 9.1% in June 2022, driven largely by post-pandemic stimulus and sharp increases across energy, goods, and services. Since then, tighter monetary policy has had its intended effect. Inflation steadily declined, reaching a low of 2.3% in April 2025, and has remained largely contained in the mid-2% range. While inflation has edged slightly higher to around 2.7%, it remains below 3%. Importantly, recent data shows that several key contributors—including dining, recreation, and other services—have begun to ease, even amid ongoing tariff implementation. Although the cumulative impact of inflation over the past several years continues to pressure household budgets, the underlying trend suggests inflation is no longer accelerating at the pace seen earlier in the cycle. Source: BLS, FactSet, J.P. Morgan Asset Management; Contributions mirror the BLS methodology on Table 7 of the CPI report. Values may not sum to headline CPI figures due to rounding and underlying calculations. “Shelter” includes owners’ equivalent rent, rent of primary residence and home insurance. “Food at home” includes alcoholic beverages. Headline and core PCE deflator inflation shown are based on seasonally adjusted data due to data availability. Official October 2025 data unavailable due to government shutdown and data shown are J.P. Morgan Asset Management estimated. Guide to the Markets - U.S Data are as of April 30, 2026.

Source: BLS, FactSet, J.P. Morgan Asset Management; Contributions mirror the BLS methodology on Table 7 of the CPI report. Values may not sum to headline CPI figures due to rounding and underlying calculations. “Shelter” includes owners’ equivalent rent, rent of primary residence and home insurance. “Food at home” includes alcoholic beverages. Headline and core PCE deflator inflation shown are based on seasonally adjusted data due to data availability. Official October 2025 data unavailable due to government shutdown and data shown are J.P. Morgan Asset Management estimated. Guide to the Markets - U.S Data are as of April 30, 2026.

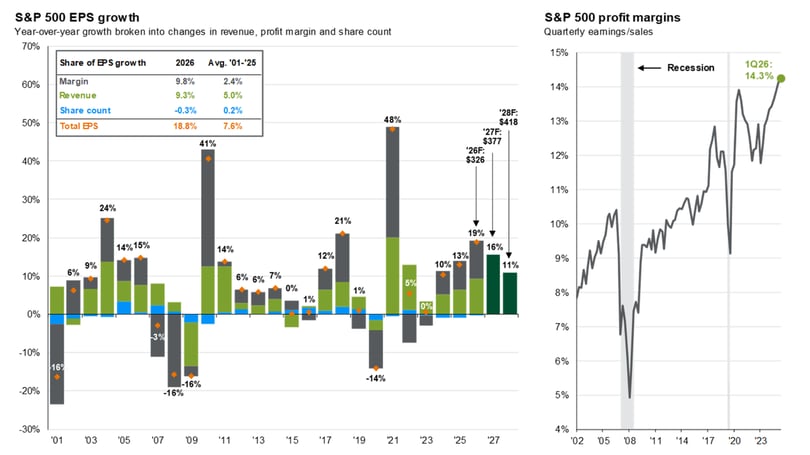

Earnings Growth Continues to Support Equities

Despite repeated recession predictions, corporate earnings have remained strong. The market continues to be supported primarily by earnings growth rather than speculative valuation expansion alone.

S&P 500 earnings growth reached approximately 13% in 2025, with analysts continuing to project double-digit growth through 2026 and beyond. Technology companies in particular continue benefiting from expanding profit margins and strong demand tied to artificial intelligence infrastructure spending.

Large technology firms are expected to spend hundreds of billions of dollars over the coming years building data centers, semiconductor infrastructure, and AI capabilities. This investment cycle continues to support earnings growth across multiple sectors of the economy.

Source: Compustat, FactSet, Standard & Poor’s, J.P. Morgan Asset Management.

Historical EPS values are based on annual earnings per share. Forecasts for 2026, 2027 and 2028 reflect consensus analyst expectations, provided by FactSet. Past performance is no guarantee of future results. Guide to the Markets – U.S. Data are as of April 30, 2026.

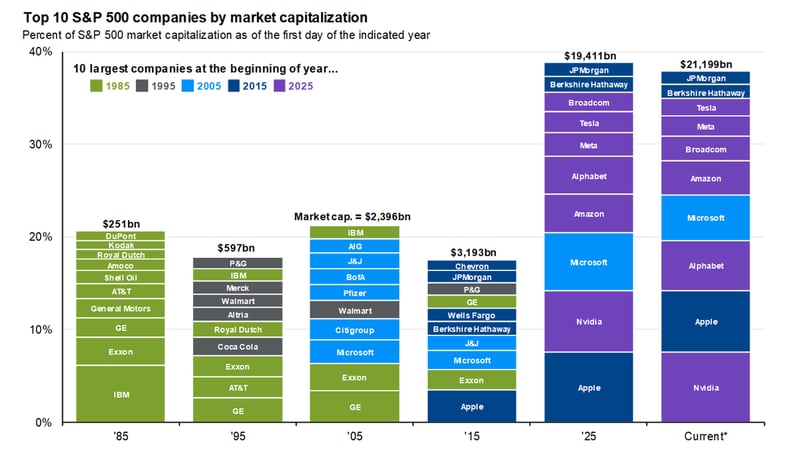

Concentration Risk Remains Elevated

While markets have remained strong overall, leadership within the S&P 500 continues to be heavily concentrated among a small number of large technology companies. Today, the top 10 holdings account for nearly 40% of the index, roughly double historical norms.

Much of this concentration has been fueled by enthusiasm surrounding artificial intelligence and the dominant positions held by major technology firms. However, history has shown that periods of extreme concentration rarely last forever, as leadership eventually rotates over time.

For investors, this reinforces the importance of diversification and avoiding the temptation to chase whichever area of the market has most recently outperformed.

Source: Bloomberg, FactSet, Standard & Poor’s, J.P. Morgan Asset Management.

Companies are organized from highest weight at the bottom to lowest weight at the top. Market weights are provided by Bloomberg through 2025 and FactSet thereafter. Past performance is no guarantee of future results.

Guide to the Markets – U.S. Data are as of May 13, 2026.

Long-Term Investing Requires Perspective

One of the clearest reminders from 2026 so far is that headlines are often poor predictors of long-term market outcomes. Financial media naturally focuses on fear, uncertainty, and short-term volatility, but markets have historically adapted through geopolitical events, economic slowdowns, and periods of uncertainty.

Over time, markets tend to follow earnings growth, innovation, productivity, and economic expansion. While volatility is inevitable, reacting emotionally to short-term headlines has historically been one of the most damaging behaviors for long-term investors.

The consistent lesson remains unchanged: maintain diversification, focus on long-term fundamentals, and avoid chasing whichever narrative or asset class has performed best most recently.

Source: FactSet, NBER, Robert Shiller, J.P. Morgan Asset Management.

Data shown in log scale to best illustrate long-term index patterns. Past performance is no guarantee of future results.

Guide to the Markets - U.S. Data are as of December 31, 2025.

For investors, the consistent takeaway remains unchanged: short-term uncertainty is unavoidable, but long-term growth has persisted. Staying disciplined, diversified, and focused on what can be controlled remains the most reliable approach to navigating evolving market conditions.

For a second look at your portfolio or investment strategy, reach out to our team.